Waiting for a crash: why Putin will wreck our prosperity (such as it is)

Waiting for a crash: why Putin will wreck our prosperity (such as it is)

Last year I became a fund manager. Not a grand one, I admit. My elevation to the world of high finance was a side effect of becoming self-employed.

I now manage my own pension, which is not a task I am qualified for. But as the cozened customers of many a financial institution have learned the hard way throughout the history of capitalism, self-styled financial experts aren’t always qualified either.

My prejudice against them was confirmed when friends, who had worked in London banks all their lives, gave me startlingly cynical advice.

“Whatever you do not trust our colleagues!” they cried.

“They will rip you off.”

I was not to hand my pension to asset managers who typically charge about 2 per cent a year. (It may not sound much but think of the compound effect as the years go by.)

I was to put it in tracker funds which charge 0.1 per cent administration fees or less. The evidence showed that tracker funds did just as well as supposedly expert fund managers.

I would be wasting my money if I gave flash bastards in tasteless suits a penny.

As someone brought up on the left with a suspicion of finance this was easy advice to take.

And then another prejudice was confirmed. Or so it seemed.

I had a small amount of money in a fund tracking the US S&P 500.

All of a sudden it started to grow. Between October and March US stocks rose by 21 percent. They’ve bounced about a bit since. But at the time of writing the S&P 500 stood at 5187 compared with 4347 six months ago.

Meanwhile European equities and the Japanese stock market have hit new highs. Even here in London, which is visibly dying as a financial centre after Brexit, the FTSE-100 is breaking records.

Surely, it’s a bubble. And surely, I should just cash in my small (and now not so small) tracker fund before it bursts.

Everything I know tells me to cash in. I have read and enjoyed the books about bubbles, which over the centuries have given readers a sense of superiority over the fools caught up in capitalist manias.

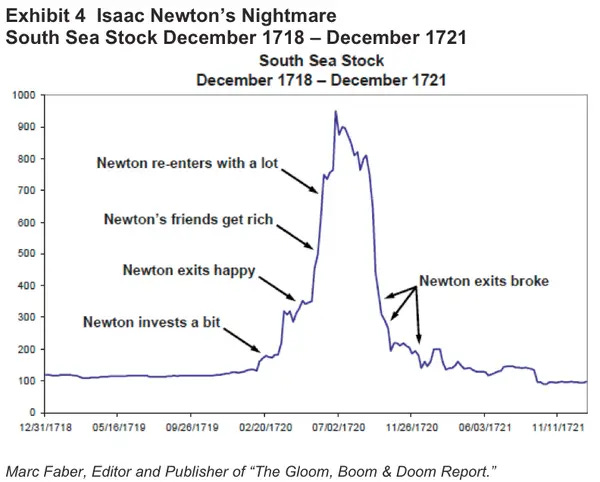

Charles Mackay’s account of the Dutch tulip mania of the 17th century and South Sea bubble of 1720, Extraordinary Popular Delusions and the Madness of Crowds, is still in print, despite being first published in 1841.

Mackay’s conclusion is so often quoted because it is often true: “Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.”

I imagine I would have laughed along with Sir Isaac Newton when he observed during the South Sea Bubble, the UK’s first capitalist mania:

“I can calculate the movement of stars, but not the madness of men.”[i]

Surely all who control their pensions should be grateful for what profits we have made and move on.

And yet, now I have control, my scoffs about the madness of crowds die on my lips. Loss aversion and fear of missing out are powerful psychological forces and I wonder if I have the strength to resist them.

The Financial Times has Stuart Kirk, an excellent investment columnist. He described how he sold his American shares in September on the sensible grounds that they could not keep rising. He noted that the price/earnings ratio for US shares was about 23 times versus an average back a century of 18 times — suggesting prices were roughly a third too exuberant.

Obviously, a fall was coming

And then, alas, he sat back and watched as the market continued to rise. “Never bet against America,” he now mutters to himself.

But perhaps you should.

Here are three reasons why you should not believe the boosters

Today’s booming markets are based on a wave of optimism about the transformative power of AI. I have no doubt it will change the world. But in all bubble markets investors are always convinced that a new technology will bring profits and productivity gains.

They are usually right. But being right doesn’t stop a crash.

The speculators behind the South Sea Bubble of 1720, who thought that slavery would bring them grotesque profits. were right. The investors who lost everything in the Wall Street Crash of 1929 were equally correct in believing that cars, radio, film and air travel were new and significant industries.

No one denies the importance of the Internet but its significance did not stop the dotcom bubble bursting at the turn of the century.

The point is not whether a new technology is important but whether investors are pouring money into lousy companies and whether exuberance and greed are out of control.

As the Economist said the other day

Bulls in the 1990s were right that advances in telecommunication would transform the world and spawn new corporate giants. Yet plenty still ended up losing their shirts—even by betting on firms that went on to be wildly successful. The canonical example is Cisco, which, like Nvidia, made hardware crucial for the new age. Although in the most recent fiscal year its net profit was $12.8bn, up from $4.4bn in 2000 (both in today’s money), those who bought shares at their peak in March 2000 and are still holding today have taken a real-terms loss of nearly 66%.

A second warning sign is that gains are concentrated in big tech companies most notably Nvidia. If it goes down, the euphoria goes down with it. Meanwhile if interest rates do not fall soon, it is easy to see pessimism rising.

The Wall Street bear David Rosenberg, the founder of Rosenberg Research, recently warned of “the air being let out of the AI balloon…The intense AI-fuelled momentum to the upside is now heading in reverse”.

Finally, look around you. We are in a pre-war world. I find it amazing that Europeans go about our lives getting and spending while all the time the worst war in Europe since 1945 grows ever nearer.

This is not the time for frivolous stock market bubbles, for exaltation and euphoria. It’s a time of fear.

I enjoy writing this newslestter. But it is a lot of work! Please consider taking out a paying subscription if you can afford to. You will have access to all articles, archives and podcasts, and you will allow me to carry on writing!

[i] Newton could not live up to his fine words. As the market rose and rose he piled back in and ended up losing everything.

Former junk bond mutual fund manager here, now trading stocks for myself.

Your suspicions are correct, Nick. As a small investor you simply do not have access to really good investment advice. The best money managers work for hedge funds. While there are certainly some reputable mutual fund companies out there, picking a good fund is tough, not much easier than picking stocks. For example, a fund with a hot track record will likely own the stocks that have performed well recently and some of those could be topping out. Fund fees also eat away at compound returns. Your assignment in picking a fund is to find sustainable performance, which is relatively rare.

As for the advice to buy and hold long term. The question is, can you stand the volatility? Stocks were down 20% or so last year, and down 45% in 2008-09, and while that doesn't happen often, you have to be prepared -- both with cash reserves and psychologically; you don't want to be forced to sell at a bottom. I've met a number of people who thought they could hold through volatility and then freaked out when reading their monthly account statements.

One more thing regarding buy and hold advice. That advice assumes unconsciously that the stability that the West enjoyed in the post WWII period will remain for the most part unimpaired. That's why buy and holders have been right consistently since the Great Depression, in their assumption that if the market tanks it will come back and make new highs if you have time and fortitude to wait out the correction. But it may not always be thus.

There are no easy answers, unfortunately.

The advice you received about using an index tracker was sound. However you should have chosen a global one, instead of investing solely in one country, even if that is the USA.

Look for a global market capitalisation weighted ETF. As investment advice is a regulated activity, I don’t name specific investments.

Trying to time the market is a mugs game.

No legal responsibility is accepted for the above comments. For background on me, visit my website which you can find from my profile or by Googling my name.